Fintech Marketing Agency & Lead Generation: How to Reach Decision-Makers in 2026

A fintech marketing agency builds compliant, targeted outbound pipelines into payment firms, neobanks, and lending platforms. Here's what it takes to generate fintech leads in 2026.

Fintech is one of the hardest B2B markets to break into. Decision-makers are sophisticated, buying committees are large, compliance requirements filter out unvetted vendors at every stage, and deal cycles routinely run 3–9 months. The cost-per-click on the keyword "fintech marketing agency" is $33.41 — one of the highest in the B2B services space — which tells you everything about the commercial pressure companies feel to solve the pipeline problem in this vertical.

This article covers what fintech B2B lead generation actually involves, why standard outbound approaches fail in this market, which channels work, how EU and US fintech outreach differ, and what to look for in a fintech marketing agency if you're considering outsourcing the function.

What Is a Fintech Marketing Agency?

A fintech marketing agency specialises in B2B lead generation and outbound sales for fintech companies, or for non-fintech vendors selling into fintech buyers. The emphasis on "fintech" is not just vertical branding — it reflects genuine specialisation in buyer behaviour, compliance constraints, messaging requirements, and channel strategies that are specific to this market.

There are two main use cases:

Fintech companies generating B2B leadsA payment infrastructure provider, neobank B2B division, lending platform, insurtech, or regtech company needs a pipeline of enterprise clients, partnerships, or distribution deals. Standard outbound agencies often lack the credibility and market knowledge to represent these brands effectively.

Non-fintech vendors selling into fintechA technology provider, IT services firm, AI company, or professional services firm targeting CTO, CPO, or VP Partnerships at payment companies, neobanks, or crypto platforms. The challenge here is penetrating a highly protective and compliance-conscious buyer base.

In both cases, a fintech marketing agency provides ICP definition for fintech sub-verticals, compliance-aware outreach infrastructure, and relationship-driven pipeline building that matches the trust thresholds of fintech procurement.What Fintech B2B Lead Generation Actually Involves

Fintech B2B lead generation is not a volume game. The buyer profile, buying process, and decision criteria all push against high-volume spray-and-pray outbound.

Buying committee sizeA fintech purchase involving technology, infrastructure, or B2B partnerships typically engages CTO or CPO (technical evaluation), CFO (commercial and risk), VP Partnerships or Head of Business Development (strategic fit), Compliance or Legal (regulatory evaluation), and sometimes a CEO or board sponsor for larger deals. You are rarely closing with one contact.

Deal timelineEven a well-qualified opportunity in fintech will take 3–9 months from first conversation to signed contract. Compliance reviews, security assessments, procurement diligence, and internal approval chains all add time. Lead generation for fintech is a pipeline investment, not a quick-win channel.

Trust thresholdFintech buyers see enormous outreach volume — particularly on LinkedIn. They are sophisticated enough to filter out generic pitches immediately. A message that works well in other B2B verticals will often fail in fintech because the credibility bar is higher. Case studies in the specific sub-vertical (not just "financial services"), named references, regulatory understanding, and specific domain knowledge in the first touchpoint all materially affect response rates.

Compliance constraints on the vendor sideSelling into a regulated industry means your outreach itself must reflect compliance awareness. GDPR compliance, data sourcing transparency, and lawful processing of prospect data are not optional for EU fintech outreach — they are a baseline expectation of buyers who operate in the same regulatory environment.

The implication for lead generation: fintech campaigns require tighter ICP definition, stronger personalisation, more account-level research per contact, and longer nurture sequences than a typical B2B outbound programme.

Why Fintech Is Different From Other B2B Markets

Most B2B markets have friction in the buying process. Fintech has friction layered on top of friction, for structural reasons that won't change regardless of how good your outreach is.

Regulation shapes every decisionWhether you're selling to a neobank in the UK, a payments processor in Germany, or a lending platform in the Netherlands, the buyer operates under regulatory oversight — FCA, BaFin, DNB, or equivalent — that makes vendors who introduce operational, security, or compliance risk unacceptable regardless of price or functionality. Trust is not a soft requirement; it is a compliance requirement.

Sub-vertical fragmentation"Fintech" is not a single market. Payment companies, neobanks, lending platforms, insurtech, regtech, wealthtech, and crypto/blockchain companies have different buyers, different procurement processes, different pain points, and different competitive landscapes. An agency claiming to serve "fintech" without sub-vertical differentiation is probably serving none of it particularly well.

Procurement processes are thoroughEnterprise fintech buyers — the ones with meaningful deal sizes — run formal vendor assessments. Information security questionnaires, legal review, reference checks, and board-level approval are standard. No amount of outreach shortcuts this process once a deal is in flight.

Integration capability matters more than featuresFintech buyers evaluate vendors heavily on integration complexity, API quality, and data architecture. Outreach that leads with features without addressing integration will stall at the technical evaluation stage.

Credibility compoundsIn fintech, a known logo in your case studies unlocks the next conversation more than any other single factor. An agency with no fintech references and no fintech-specific messaging is operating at a significant disadvantage even with strong general outbound capability.

Channels That Work in Fintech Lead Generation

LinkedIn: Primary Channel for Fintech B2B

LinkedIn is where fintech B2B relationships are built. Decision-makers at payment companies, neobanks, and lending platforms are demonstrably active — senior fintech professionals post, engage, and respond to messages at higher rates than in most other verticals. This is not a coincidence: fintech operates in a relationship-intensive market where personal credibility travels before commercial conversations begin.

What works on LinkedIn for fintech:

- Warm connection + content sequence: Building presence in a sub-vertical community before reaching out commercially. Decision-makers in fintech check profiles before accepting connections; a profile with relevant content and engagement signals domain credibility.

- Stakeholder mapping per account: Connecting with 2–3 stakeholders at target accounts rather than a single contact. The partnership decision typically involves the commercial lead and at least one technical or compliance stakeholder.

- Conversational, not pitchy: Fintech buyers respond to messages that demonstrate they've been read — specific reference to the company's product, market position, or recent news. Generic templates perform poorly.

Cold Email: Secondary but Essential

Cold email works in fintech when the message is highly targeted and the data quality is verified. The failure mode is high volume, low personalisation, and non-compliant data sourcing — all of which are more likely to backfire in fintech than in less regulated verticals.

What works:

- Verified, GDPR-compliant contact data with lawful basis for processing

- Short, specific emails referencing the prospect's specific situation — not boilerplate about "helping fintech companies"

- Clear, credible sender identity and domain infrastructure (fintech buyers check sender reputation)

- Sequences of 3–5 touches maximum; excessive follow-up damages credibility in this market

What doesn't work: scraped lists, generic "I help financial services companies" messaging, and high-frequency automated sequences that feel like marketing noise.

Conferences and Events: High ROI, High Cost

Money20/20 (Amsterdam and Las Vegas), Finovate, Sibos, and regional fintech summits are the concentrated meeting grounds for fintech decision-makers. Conference lead generation in fintech produces some of the highest-quality pipeline because the context signals interest, the in-person format builds trust faster, and the meeting density is high.

The challenge is cost. Conference attendance and side-event hosting require significant investment relative to per-meeting cost of digital outreach. For companies with deals of €50K+ ACV, conference pipeline activity makes strong economic sense. For smaller deal sizes, digital channels deliver better ROI.

The best programme combines all three: multi-channel B2B lead generation with LinkedIn as the primary relationship channel, email as the follow-through mechanism, and conference activity for highest-value targets.

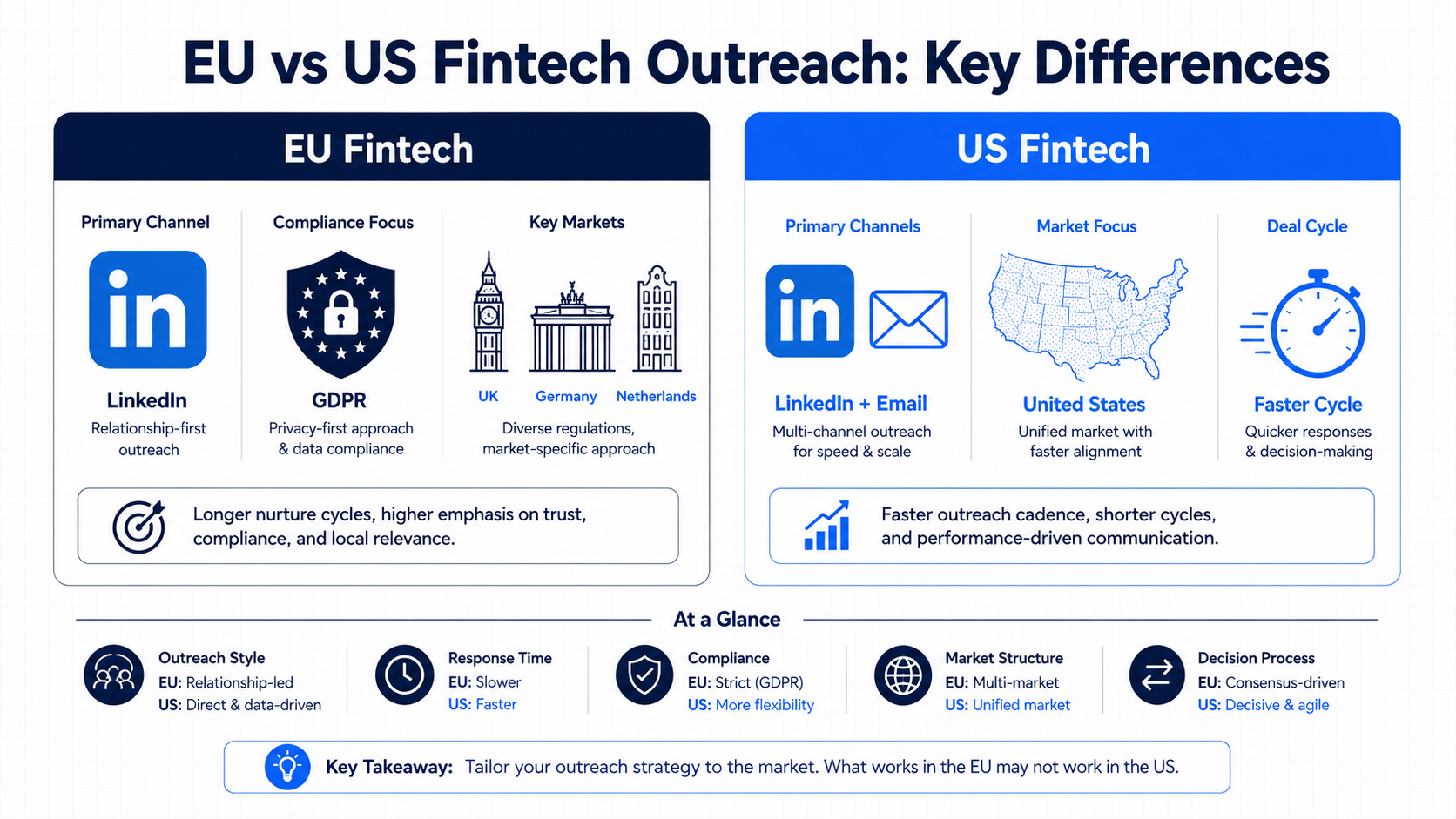

EU vs US Fintech Outreach: What's Different

Fintech is a global market, but the rules of engagement differ materially between EU and US buyers.

| Dimension | EU Fintech Buyers | US Fintech Buyers |

|---|---|---|

| Primary channel | LinkedIn first | LinkedIn + cold email roughly equal |

| Cold calling | Very low tolerance | Moderate acceptance |

| Data compliance | GDPR mandatory | CAN-SPAM minimum; CCPA in California |

| Decision speed | Slower; consensus-driven | Faster at Series A–B scale |

| Trust signals | Local case studies, EU regulation familiarity | US references; thought leadership |

| Key markets | UK, Germany, Netherlands, Nordics, Baltic states | New York, San Francisco, Miami |

| Procurement style | Formal; compliance-led | Pragmatic; commercial-led |

| Response to personalisation | High — research is expected | High — but less focused on regulatory fit |

When to Hire a Fintech Marketing Agency

Hiring a specialist fintech lead generation agency makes sense under specific conditions:

You're entering a new sub-verticalMoving from payment technology into neobank partnerships, or from IT services into regtech — requires sub-vertical credibility you don't yet have internally. An agency with active campaigns in that sub-vertical reaches buyers faster and with less reputation risk.

Your internal team lacks fintech-specific outreach experienceGeneric SDR capability produces poor results in fintech. Messaging that doesn't address compliance, integration, or sub-vertical specifics will be filtered out. If your existing outbound team hasn't built fintech pipeline before, the learning curve is expensive.

You need EU market penetration with GDPR complianceSetting up GDPR-compliant outbound infrastructure — data sourcing, lawful basis documentation, opt-out management, sending domain warm-up — requires specific expertise. An EU-based agency with established infrastructure can launch in weeks rather than months.

Deal cycles are long and you need pipeline nowAt 3–9 month deal timelines, a 6-month delay in starting outbound means a 6-month delay in first revenue. Outsourcing to an experienced provider compresses the time to first qualified meetings from 3–6 months (for an in-house build) to 4–6 weeks.

You're preparing for a conference and want pre-booked meetingsRunning a pre-conference outreach campaign to book 15–25 meetings at Money20/20 or Finovate is one of the highest-ROI outbound activities available to fintech companies. It requires compressed timelines and event-specific sequencing that a specialist handles more effectively than a general SDR team. Conference lead generation is a distinct capability.

VirtuWise: Fintech Lead Generation for EU, UK, and US Markets

VirtuWise runs outbound pipeline programmes for B2B companies selling into and within fintech — including payment companies, neobanks, lending platforms, insurtech, regtech, wealthtech, and crypto/blockchain.

What the fintech engagement includes:- ICP definition and account targeting across fintech sub-verticals (neobanks, payments, lending, insurtech, regtech, wealthtech, crypto)

- Stakeholder mapping: CTO, CPO, CFO, VP Partnerships, Head of Business Development

- LinkedIn outreach as primary channel with compliance-aware messaging

- GDPR-compliant EU data sourcing with lawful basis documentation

- Cold email infrastructure with verified sending domains and bounce management

- Multi-stakeholder sequencing for enterprise fintech accounts

- Pre-conference meeting booking for Money20/20, Finovate, and regional events

- Weekly campaign reporting with response analysis and messaging optimisation

- Lead Generation — €3,000/month: LinkedIn-first single-channel outbound, 1 campaign

- Lead Generation Plus — €5,000/month: Multi-channel (LinkedIn + email), broader ICP coverage

- Business Development — €7,000/month: Full-cycle engagement with dedicated BDR, multi-stakeholder campaigns, conference support

How to Evaluate a Fintech Marketing Agency

1. Ask for sub-vertical specificity, not "fintech" generalism

Any agency can claim fintech experience. Ask which sub-verticals they have active campaigns in, which titles they routinely reach, and what their messaging approach is for compliance-sensitive buyers. An agency without specific answers here is selling general outbound with a fintech label.

2. Verify GDPR compliance infrastructure for EU campaigns

Ask specifically about data sourcing — where contact data comes from, what lawful basis is documented for EU outreach, how opt-outs are managed, and whether they can provide a data processing agreement. In fintech, a prospect who receives non-compliant outreach from a vendor will not just ignore it — they may actively report it. EU compliance capability is not optional.

3. Check LinkedIn capability versus email-only providers

Fintech B2B lead generation requires LinkedIn as the primary channel. An agency that runs email-only campaigns is missing the most important channel in this market. Ask what percentage of their fintech meetings come from LinkedIn versus email, and whether they manage LinkedIn outreach through client profiles or separate channels.

4. Evaluate their understanding of fintech buying cycles

An agency that promises meetings "within 2 weeks" without acknowledging 3–9 month deal cycles in fintech does not understand the market. Quality fintech lead generation builds pipeline measured in quarters, not immediate pipeline close. Ask how they report on pipeline at different stages and how they handle long-cycle accounts.

5. Assess the reporting structure for multi-stakeholder accounts

For enterprise fintech targets with multiple stakeholders, you need account-level visibility: which contacts have been reached at each account, what responses have been received, which accounts have active conversations. An agency reporting only lead counts and meeting volumes lacks the visibility to manage enterprise fintech pipeline correctly.

Frequently Asked Questions

What does a fintech marketing agency do?A fintech marketing agency runs outbound lead generation and pipeline building specifically for fintech companies or vendors selling into fintech. This includes ICP definition for fintech sub-verticals, LinkedIn outreach, GDPR-compliant cold email, multi-stakeholder engagement at payment companies and neobanks, and event-based meeting generation at fintech conferences.

What is fintech lead generation?Fintech lead generation is the process of identifying and engaging qualified prospects at fintech companies — including payment processors, neobanks, lending platforms, insurtech, regtech, wealthtech, and crypto/blockchain companies — through outbound channels (LinkedIn, cold email, events) to produce qualified sales conversations and pipeline.

Who are the decision-makers in fintech B2B sales?Fintech B2B buying committees typically include: CTO or CPO (technical evaluation and integration), CFO (commercial and risk), VP Partnerships or Head of Business Development (strategic fit), Compliance or Legal (regulatory review), and CEO for larger deals. Effective fintech outreach engages at least 2–3 stakeholders per account rather than relying on a single contact.

How long is a typical fintech B2B sales cycle?Fintech deal cycles typically run 3–9 months from first qualified conversation to signed contract, depending on deal size, the number of stakeholders involved, and the complexity of compliance and security reviews. Enterprise fintech deals (€100K+ ACV) can extend to 12 months. Pipeline built today typically converts in Q3–Q4.

Is LinkedIn effective for fintech lead generation?Yes — LinkedIn is the primary channel for fintech B2B outreach, particularly in EU markets. Senior fintech decision-makers (CTO, VP Partnerships, Head of BD at neobanks and payment companies) are demonstrably active on LinkedIn. Response rates on well-personalised LinkedIn outreach in fintech are meaningfully higher than cold email in most EU sub-verticals.

What does GDPR-compliant fintech outreach look like in practice?GDPR-compliant B2B outreach relies on legitimate interest under Article 6(1)(f) as the lawful basis. This requires: contact data sourced from lawful B2B databases (not consumer-origin scraped data), genuine assessment that the individual's role makes them a relevant prospect, a clear opt-out mechanism in every outreach, and documented lawful basis records. In fintech, compliance-aware outreach is both a legal requirement and a commercial signal — fintech buyers are more likely to respond to outreach they can see is professionally structured.

The Bottom Line

Fintech is not a B2B vertical where generic outbound produces results. The buyers are sophisticated, the buying committees are large, the compliance requirements filter vendors aggressively, and deal cycles run long. The companies generating qualified fintech pipeline consistently are doing so with sub-vertical specialisation, multi-stakeholder engagement, LinkedIn-first channel strategy, and GDPR-compliant EU data infrastructure.

The $33.41 CPC on "fintech marketing agency" reflects how commercially valuable it is to solve this problem — and how difficult it is to solve it without the right expertise. Companies that figure out fintech outbound gain a compounding advantage: early pipeline builds the case studies and references that make the next wave of outreach more effective.

Whether you're a fintech company building a B2B partnership pipeline, or a technology vendor trying to break into the neobank and payments ecosystem, the principles are the same: tight ICP definition at sub-vertical level, credibility-first messaging, LinkedIn as the primary channel, and patience with the timeline. The companies that treat fintech pipeline as a 12-month investment consistently outperform those chasing short-cycle volume metrics.

Ready to build a fintech outbound pipeline? VirtuWise runs GDPR-compliant multi-channel lead generation for B2B companies in EU, UK, and US fintech markets — from €2,500/month. View our services, see pricing, or explore our LinkedIn lead generation approach.

Related reading: - B2B Lead Generation Channels in 2026: What Works and What Doesn't - Conference Lead Generation for B2B: How to Fill Your Calendar at Industry Events - Account Based Marketing Agency: What ABM Is, What It Costs, and When You Need One - Inside Sales Outsourcing: What It Is, When It Works, and How to Do It Right (2026)